BAI Index: Peak blinders: Elevated inventories likely keep a lid on rates, but maybe not

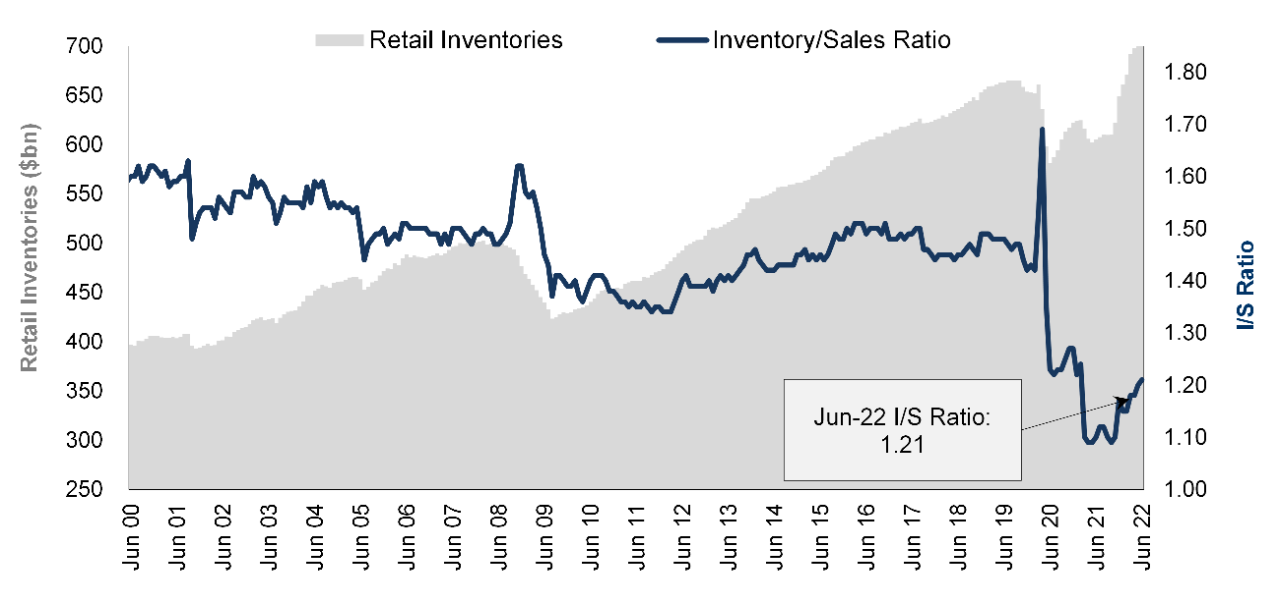

We’ve heard profit warnings and anecdotes of elevated inventories at several large U.S. retailers, and on an absolute basis, we see that in the inventory data (Exhibit 1).

Exhibit 1: U.S. Retailer inventory-to-sales ratios remain depressed, but absolute inventories continue to climb to record levels.

Source: U.S. Census Bureau; Stifel format

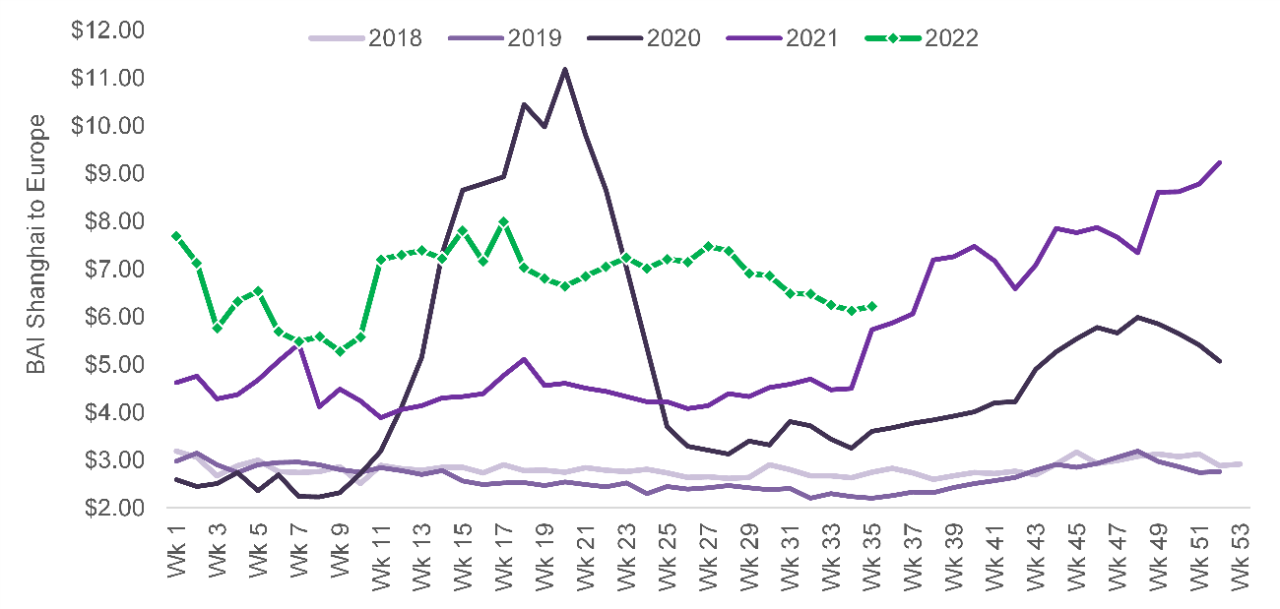

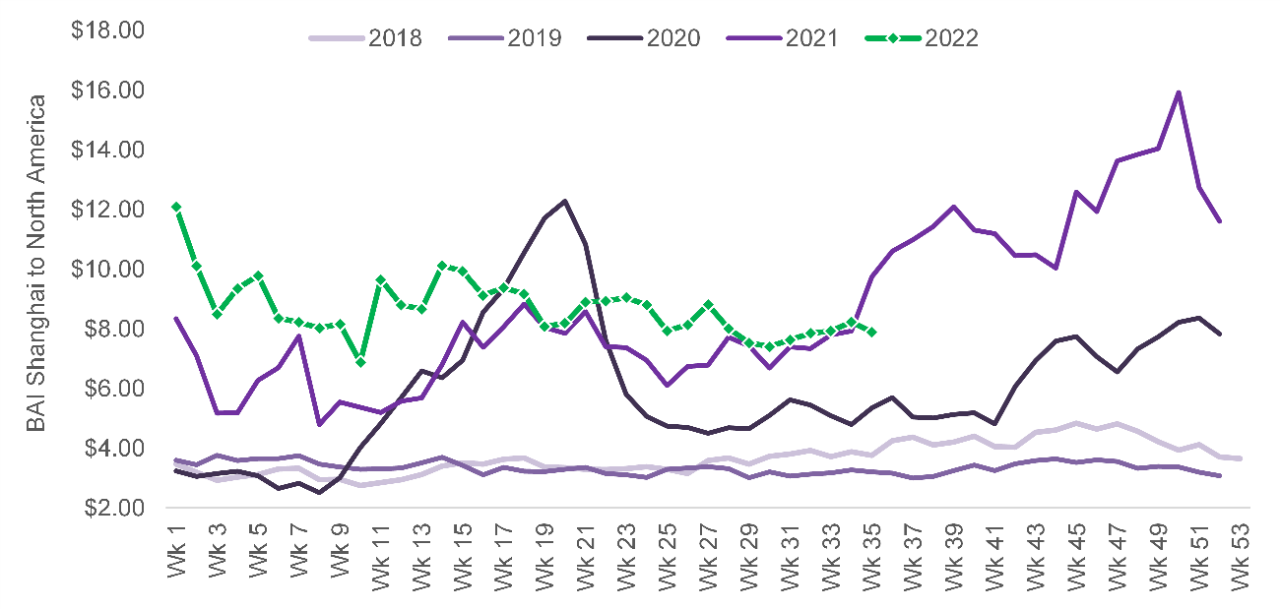

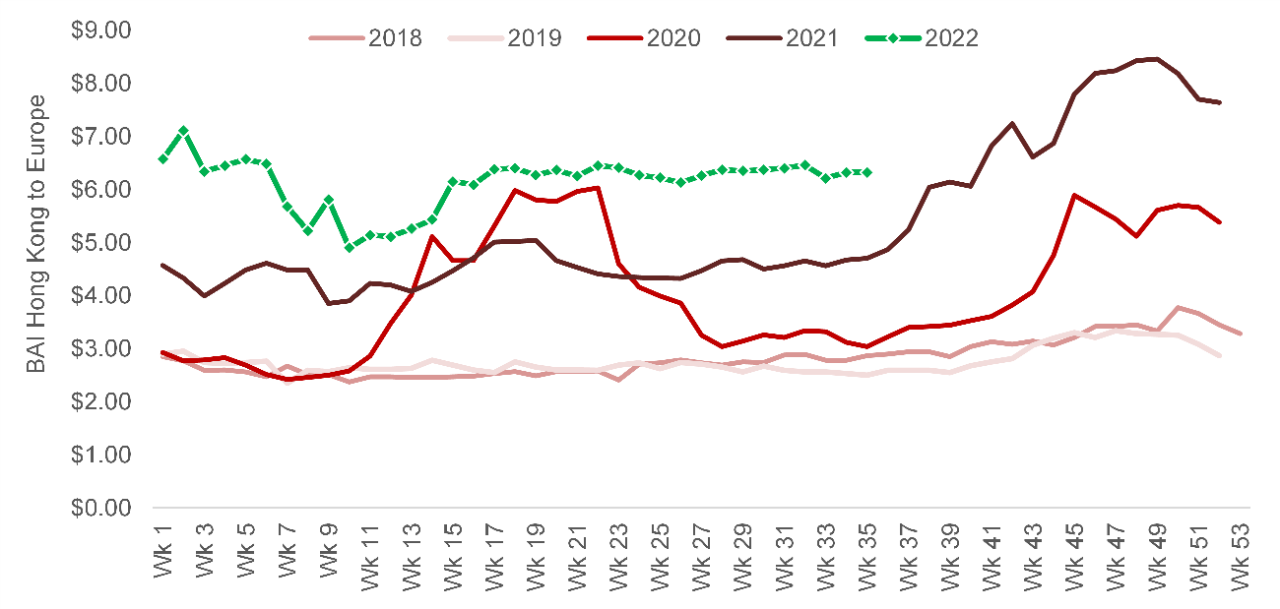

There is a possibility that these anecdotes and the inventory data are not telling the full story (more on this later), but we are seeing some early corroboration from reported BAI air cargo pricing. USD per kilo rates have been remarkably steady this year on all major Asia-outbound lanes, including Shanghai to Europe and North America, respectively, and Hong Kong to Europe and North America, respectively. But around this time in 2021, we first started seeing notable and steady rate build into the middle of the fourth quarter, as 1) demand was strong, 2) supply chains were very congested, and 3) inventories remained low.

In any case, rates remain sequentially flat (at a high level), but year-on-year comps are turning negative against the very pronounced pricing run-up toward the end of 2021.

Trends in 2022 point to looser capacity on all three of those counts, with 1) some softening in consumer demand and consumer demand indicators, 2) more supply-chain fluidity, albeit in a still-constrained system, and 3) better and more preparation from shippers -especially large ones, with earlier build-up of inventory. On this latter point, we think it is important to point out that there has been some bifurcation of inventory strategy, with large retailers able to amass more buffer stock -and perhaps too much -while smaller retailers, brands, and industrial shippers are still struggling to normalize their inventories. In any case, rates remain sequentially flat (at a high level), but year-on-year comps are turning negative against the very pronounced pricing run-up toward the end of 2021 (see Exhibit 2).

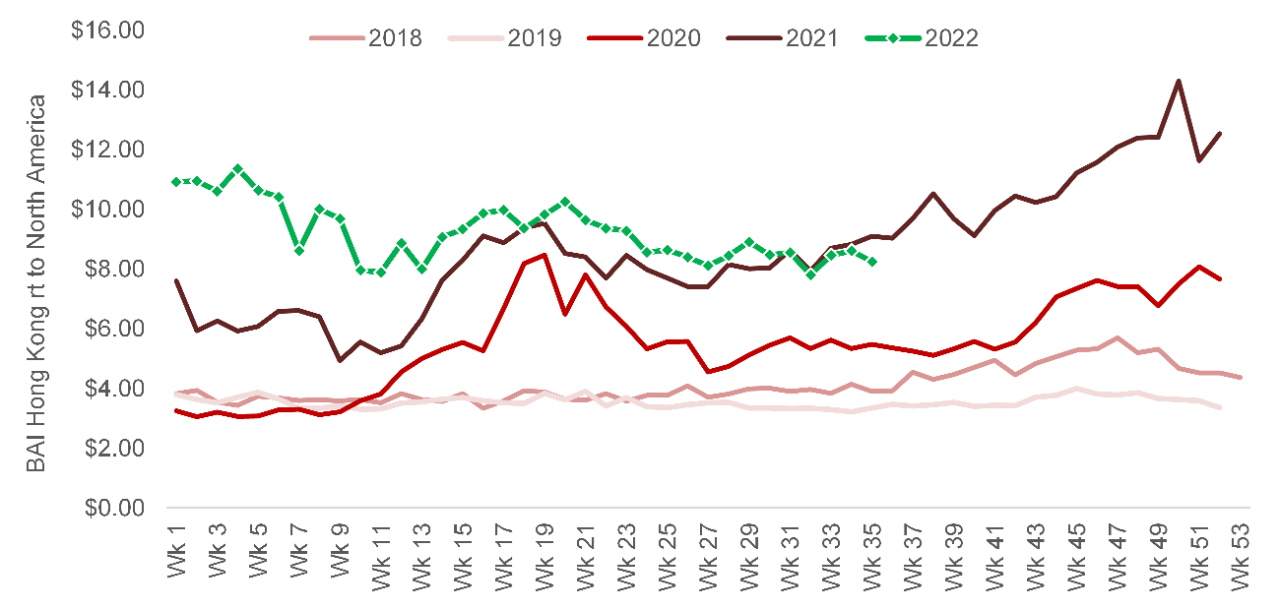

Exhibit 2: Rates have held steady all year on Asia Outbound lanes, including Shanghai-Europe (BAI81), Shanghai-North America (BAI82), Hong Kong-Europe (BAI31), and Hong Kong-North America (BAI32). More muted demand, more supply chain fluidity, and higher relative levels of stock may mean we miss the run-up in cargo rates that we experienced last year.

Source: BAI data, Stifel format

So where could this thesis on a widening spread in 2021 and 2022 back half rates be wrong? Well, first, as we pointed out earlier, the “elevated inventory” story is not perfectly representative of the entire market. Current efforts by retailers to clear stock via discounting may pave the way for late-peak replenishment, in turn producing a corresponding spike in pricing later in the season. Macro factors like consumer demand, energy prices, and geopolitical developments weigh heavily on the range of outcomes, and we think many shippers are securing capacity out of an abundance of caution, which also could be helping to support pricing. Persistent congestion in the supply chain is another factor that’s helping to keep absolute rates stable: ongoing port bottlenecks; labor challenges in the U.S. and Europe in ocean, rail, and trucking; continued labor scarcity; and the potential for climate and geopolitical shocks to energy prices to name a few.

As we said last month, we believe we’ve seen peak freight volumes. Rates are likely to remain stable or grind directionally lower. The spread between current rates and year-over-year pricing should continue to moderate.

As we said last month, we believe we’ve seen peak freight volumes. Rates are likely to remain stable or grind directionally lower. The spread between current rates and year-over-year pricing should continue to moderate. The long-term trend is reversion toward mean, with the key question being how fast and to what degree. But the market is by no means predictable, in our view, especially near term. There could be sudden rate shocks, which are probably more likely to the upside (for demand reasons) than the downside (given supply constraints) at least for the duration of this year.

About Bruce Chan, Director & Senior Analyst, Global Logistics & Future Mobility Equity Research, Stifel

Bruce Chan joined Stifel in 2010 and is based out of the Miami office.

Bruce Chan can be reached at chanb@stifel.com. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation or needs of individual investors. For more information and current disclosures for the companies discussed herein, please go to the research page at www.stifel.com.

©2022 by J. Bruce Chan.