BAI Index November 2023: Deck the Hulls: It’s Beginning to Look a Lot Like Christmas, but Still Too Early to Get Too Jolly

Consensus expectations have been for a “flat-to-slightly-up” year-over-year (y/y) peak season and our recent conversations with shippers and service providers across the freight ecosystem have been corroborating that view. In addition, the latest BAI airfreight rate data seems to do so as well.

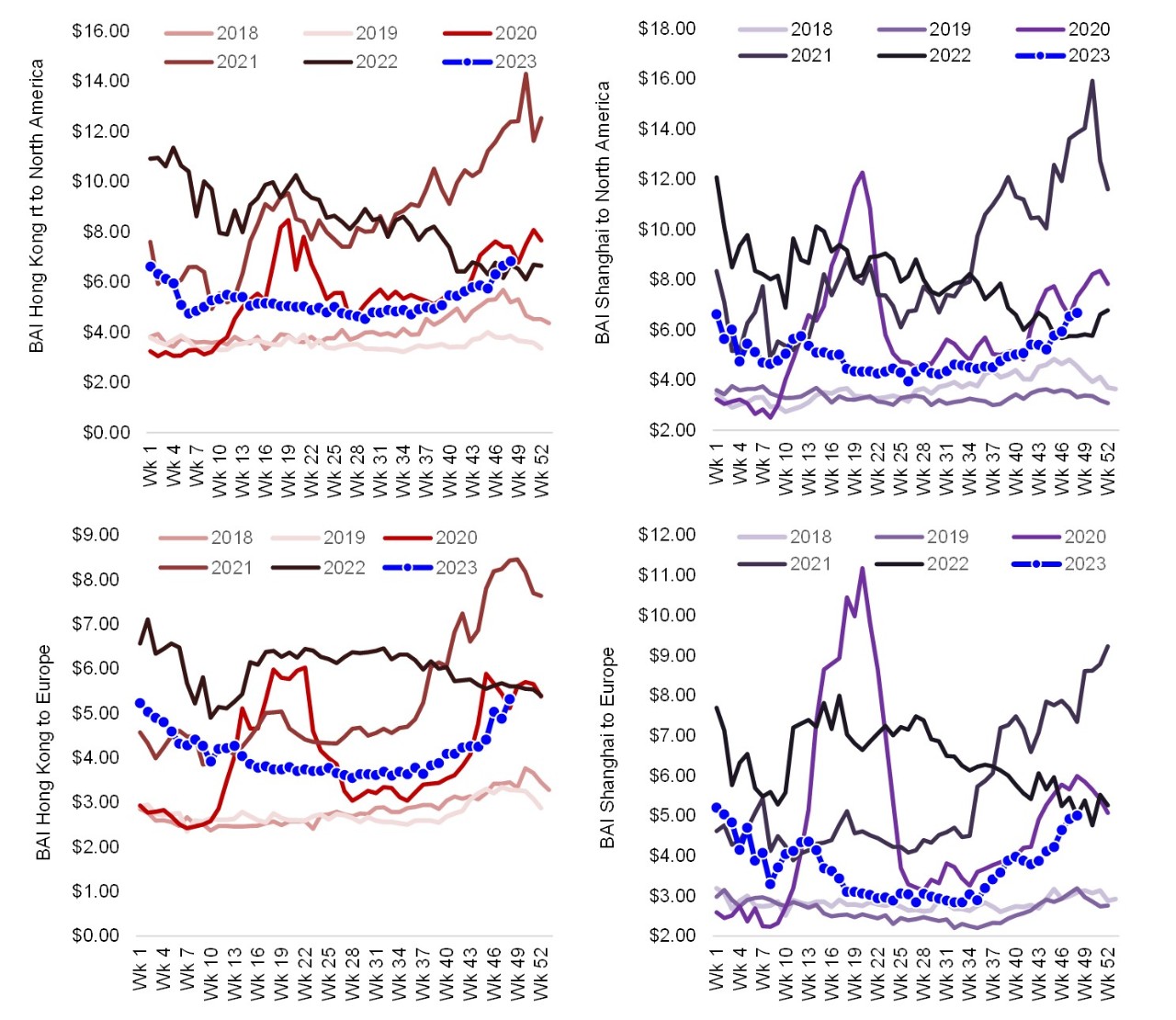

November saw a steady upward trend through the month, heralding a return to normal seasonal patterns after a very abnormal post-pandemic period. In week 48, y/y declines in Hong Kong to Europe rates were only 5%, while on the Shanghai to Europe lane, rates were flat. Meanwhile, on the Hong Kong to North America and Shanghai to North America routes, week 48 rates increased 2% and 16%, respectively.

On a monthly basis, the average rate per kilo in November was down approximately 30% y/y from both Hong Kong to Europe (BAI 31) and Shanghai to Europe (BAI 81), and down 17% and 18% y/y from Hong Kong to North America (BAI 32) and Shanghai to North America (BAI 82), respectively. However, the average monthly comparison doesn’t tell the full story, in our view. November saw a steady upward trend through the month, heralding a return to normal seasonal patterns after a very abnormal post-pandemic period. In week 48, y/y declines in Hong Kong to Europe rates were only 5%, while on the Shanghai to Europe lane, rates were flat. Meanwhile, on the Hong Kong to North America and Shanghai to North America routes, week 48 rates increased 2% and 16%, respectively.

While the recovery in BAI air cargo rates this month has been encouraging and we continue to see a return to normal seasonal patterns, capacity is still plentiful and will remain a headwind to rates for the foreseeable future. Ultimately, freight demand trends need to improve more, but for now, they remain fragile.

These are encouraging signs and as we discussed last month, strong e-commerce activity out of Asia seems to be driving a large chunk of the capacity demand. Indeed, Cyber Week sales in the United States climbed a robust 8% y/y. That’s generally good news for air cargo service providers, but we think it is too early to extrapolate this trend to a broader economic recovery. For one thing, we believe some of the cyber activity, at least in the US, was a product of attractive “door buster” deals. Moreover, broader retail sales performance was much more muted and, net of inflation, were likely even slightly more negative y/y.

According to IATA, air cargo demand has improved and was up for three consecutive months as of October, but as we’ve been discussing for most of the year, capacity - in particular air cargo belly capacity - continues to increase at a faster rate. Global available cargo tonne-kilometers (ACTKs) climbed over 13% y/y, while cargo tonne-kilometers (CTKs) increased about 4% y/y. The supply-demand discrepancy was even more pronounced in the Asia-Pacific theater, where CTKs increased 7.6% y/y in October and ACTKs were up a full 30%. While the recovery in BAI air cargo rates this month has been encouraging and we continue to see a return to normal seasonal patterns, capacity is still plentiful and will remain a headwind to rates for the foreseeable future. Ultimately, freight demand trends need to improve more, but for now, they remain fragile.

Exhibits 1-4: Rates on Asia outbound lanes increased throughout November for a relatively late seasonal push; the market appears to have resumed normal patterns, but we remain cautious given numerous demand risks and continued capacity growth

Source: Baltic Air Freight Index, Stifel Format

About Bruce Chan, Director and Senior Research Analyst covering Global Logistics and Future Mobility, Stifel

Bruce Chan joined Stifel in 2010. Based out of the Miami office, Mr. Chan is a Director and Senior Research Analyst covering Global Logistics and Future Mobility.

Bruce Chan can be reached at chanb@stifel.com. Opinions expressed are subject to change without notice and do not take into account the particular investment objectives, financial situation or needs of individual investors. For more information and current disclosures for the companies discussed herein, please go to the research page at www.stifel.com.

©2023 by J. Bruce Chan.