A forward contract is a type of derivative contract obligating counterparties to buy or sell an asset at a specified price on a future date.

Today, Forward Freight Agreements (FFAs) are contracts that give the contract owner the right to buy or sell the freight price for future settlement. An FFA, however, is a purely cash-settled contract with no physical delivery attached (a contract for difference or CFD). The underlying market is based on the spot freight indices produced by the Baltic Exchange for each respective trade.

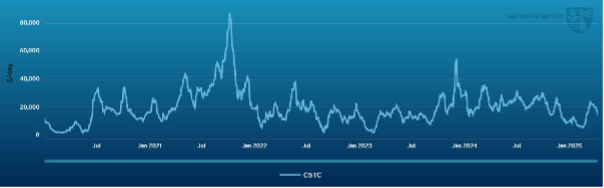

Baltic Exchange Capesize 5TC Average:

High volatility seen in the physical freight market has led participants to search for hedging opportunities within the FFA market as part of their day-to-day risk management strategies.

FFAs are traded Over the Counter (OTC), meaning they are facilitated by a broker, and are given up for clearing to an exchange. In the freight market, clearing is provided by: CME (Chicago Mercantile Exchange), EEX (European Energy Exchange AG), ICE (Intercontinental Exchange) and SGX (Singapore Exchange).

Please click here for more information on The Role of the Clearing Exchange.

Typical FFA market participants will include the following:

Shipowners:

Their risk factors include a future change in demand for their vessels which may adversely affect the cash-flow required to finance the vessels. Trading FFAs will mitigate this future risk and is a form of hedging. They may also use FFAs to create an exposure to markets where they currently do not have any physical assets. Furthermore, FFAs can be traded to take advantage of higher freight levels to maximise cash-flow.

Cargo Owners:

Correspondingly, they face the risk of a future change in ocean transportation supply which may affect their sales margins and other factors. They can utilise FFAs to aid in the protection of their projected P&L position, looking to lock in shipping costs when freight levels are low.

Portfolio players / Operators:

Their business means they will be exposed to the risk of a future change in both freight supply and demand and will trade FFAs to manage this. They are also likely to trade opportunistically (speculative trading).

Banks / Financial institutions:

They will typically trade on behalf of their clients, using FFAs not only to mitigate future changes in supply and demand, but also perhaps to secure stable ship finance cash flows.

Funds:

They may be looking for exposure into the shipping market without owning a ship or buying shipping equity, or managing client interests, both institutional and retail.