FFAs are constructed for the purposes of Risk Management which can take several forms, including:

Hedging:

If you hold a position in the underlying physical freight market and wish to reduce the risk associated with adverse market price fluctuations, you can effectively hedge that physical market position by trading the opposite position in the most closely correlated FFA market.

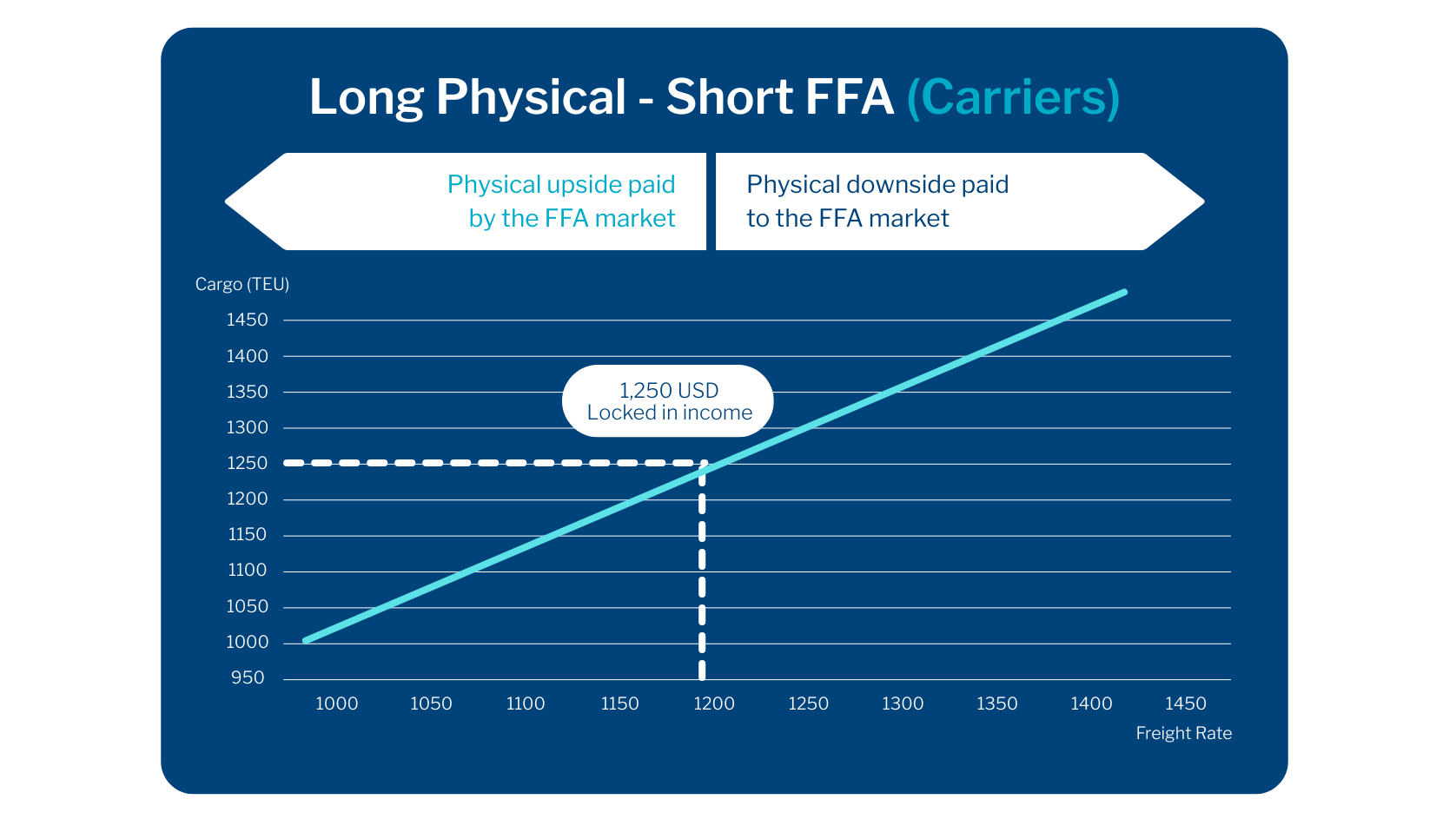

Put in simple terms, if you are a Shipowner, you are considered long freight i.e. you have possession of the physical freight (ships) and will be concerned with the value of freight falling. Therefore, in the forward market you will hedge by selling a forward contract – creating an opposing short position.

Example of a seller of container FFAs:

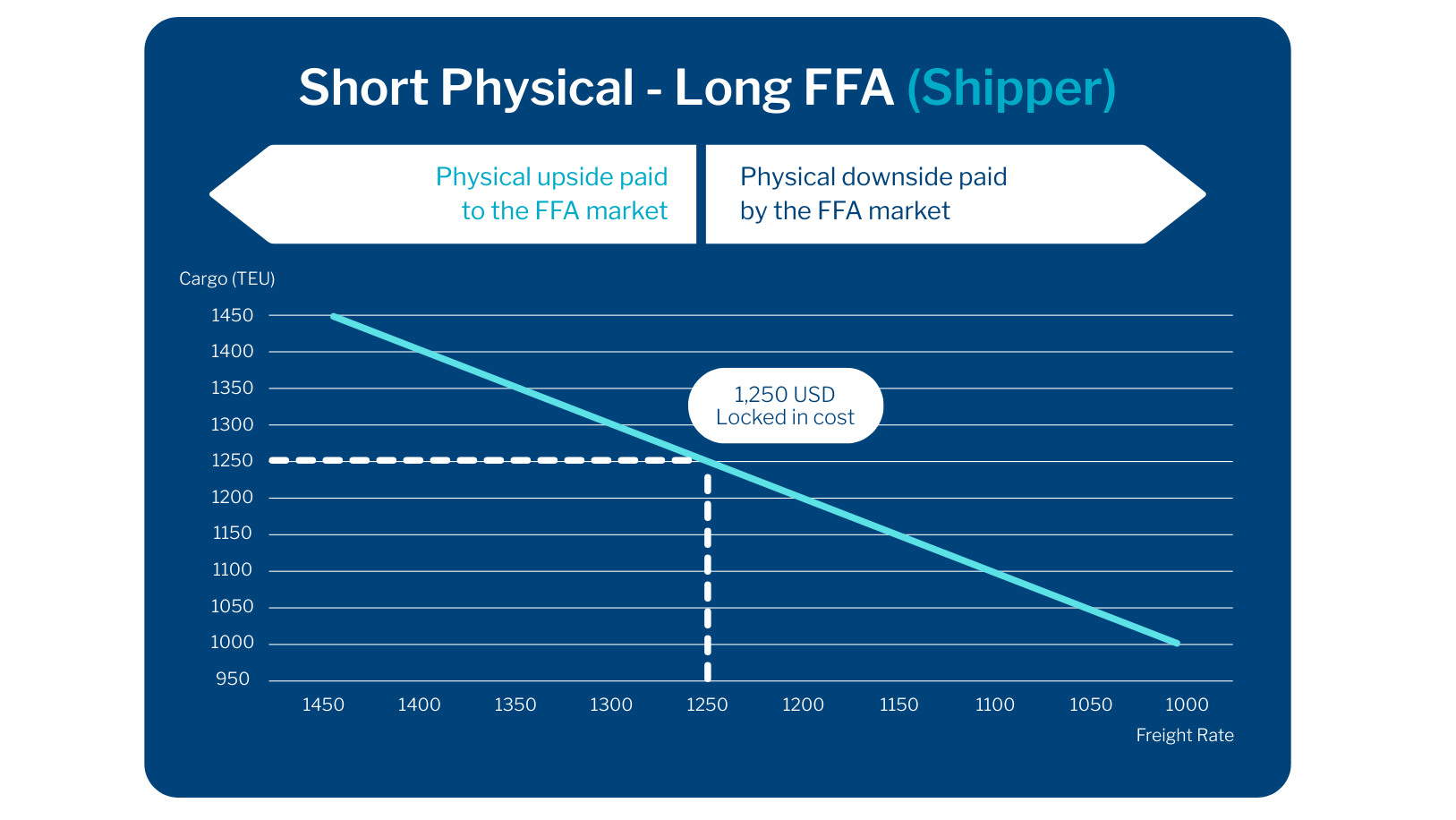

Similarly, a Cargo Owner is considered being short freight; they are seeking physical freight cover and will be concerned with the effect of freight rising. They will hedge by buying a forward contract – creating an opposing long position.

Example of a buyer of container FFAs:

Speculation:

This is employed by those without a position in the underlying physical freight market looking to maximise returns through the successful anticipation of freight movements.

Trading Opportunity and Arbitrage:

There are also opportunities to create returns by trading combinations of strategies such as calendar spreads (for example selling one time period and buying another simultaneously), size spreads (for example trading between vessel sizes e.g. on dry, cape vs panamax markets) or even geographical spreads (for example the Atlantic vs the Pacific) etc.

It may also be possible to create hybrid routes, composed of different underlying component routes i.e. combining FFA products to create a proxy most aligned to the physical route required.

An arbitrage trade seeks to return a profit by taking advantage of the price differences in a contract between similar markets or products.

Cash flow security:

This might be required in instances related to physical ship finance to provide a secure and stable minimum freight income going forward.

Forward Curve:

The forward curve provides a user with the market participants’ valuation of the future spot price, on that day, for each contract time period, e.g. the front month, or Q3 next year, or the full Calendar price etc. This provides valuable visibility of potential freight costs and is therefore a handy tool to negotiate and secure freight income and control freight costs.

The terms contango or backwardation are often used in relation to the forward curve. Freight forward curves can show a market in backwardation where the forward price of the futures contract is lower than the spot price. A trader may try to use this to their advantage by selling the front months and buying the lower priced forwards.

Conversely, a curve in contango shows future prices trading at a premium to the spot price and trading strategies will take this into consideration.

Forward curves move throughout the year between showing markets in contango and backwardation; this can be related to seasonality or other events in the underlying physical market.