BAI Index June 2026: After Iran war shock, air freight rates ease a little in May – but remain elevated

After the dramatic increases of March and April, air freight rates eased a little lower during May, according to the latest data from TAC Index, the leading price reporting agency on air freight rates and calculating agent for the Baltic Air Freight indices.

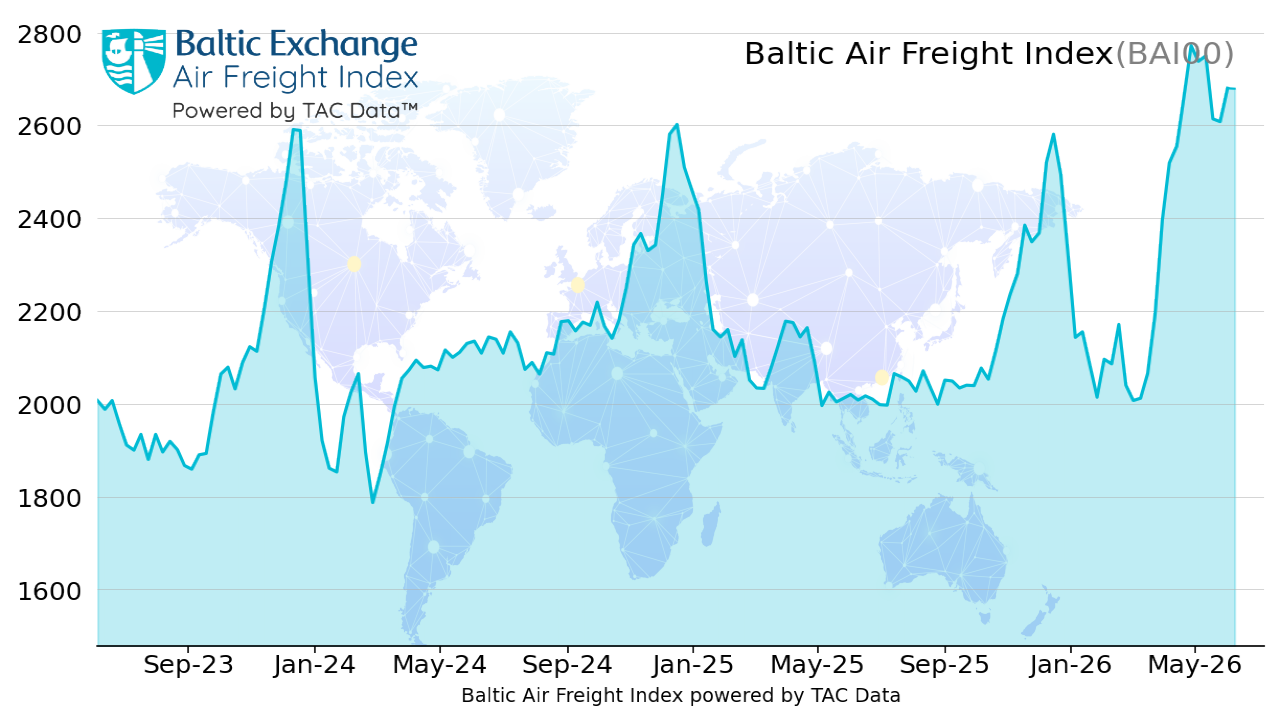

The global Baltic Air Freight Index (BAI00), calculated by TAC, drifted lower by -2.1% over the four weeks to 1 June, leaving it up some +32.7% from 12 months earlier, which is still above levels only seen in recent years at the height of peak season. After a flat first week of June, it was still higher year-on-year (YoY) by some +33.4%.

As usual, however, the headline numbers mask a rather more complicated underlying picture.

One key development helping to ease pressures on the market in May was a steady and significant fall in jet fuel prices, which had escalated alarmingly over the previous two months after the start of the US/Israel war with Iran.

One key development helping to ease pressures on the market in May was a steady and significant fall in jet fuel prices, which had escalated alarmingly over the previous two months after the start of the US/Israel war with Iran.

By 29 May, jet fuel prices had fallen back -24.8% from the previous month’s average, according to Platts data published via the IATA Jet Fuel Price Monitor. That was clearly a marked improvement, although still a massive +57.3% above the previous year’s average and with prices firming up again in the first week of June.

Various factors were at play in this easing of jet fuel prices. Firstly, there were at least 12,000 flight cancellations announced during May – led by big airlines such as Lufthansa, Turkish and China Eastern plus a long list of others – which helped trim some demand for jet fuel (as well as some bellyhold capacity).

The United States and other Western countries had also already moved to ease the pressure on supplies by releasing crude oil from strategic reserves.

Meanwhile, there were reports that China – a big refiner of crude oil into products like jet fuel – had lifted an apparent ban on jet fuel exports imposed at the start of the Iran war, at least to neighbouring countries in Asia that rely on China as their leading supplier.

All of that said, overall rates may have come off recent highs but remained extremely elevated, with sources wondering how long jet fuel prices could keep falling if inventories continued to decline.

BAI Spot rates from Hong Kong to Europe barely moved down at all over the month, from HK$45.50 per kilo on 30 April to HK$44.54 on 29 May and edging up again by early June.

BAI Spot from HK to the US also eased a little in May but not much. HK to the US East Coast dipped from HK$57.53 per kilo on 30 April to HK$55.54 by 29 May but was rising again in early June. Similarly, HK to the US West Coast eased a little from HK$53.96 to HK$51.71 between the same dates but was also rising in early June.

BAI Spot from HK to the US also eased a little in May but not much. HK to the US East Coast dipped from HK$57.53 per kilo on 30 April to HK$55.54 by 29 May but was rising again in early June. Similarly, HK to the US West Coast eased a little from HK$53.96 to HK$51.71 between the same dates but was also rising in early June.

Meanwhile, BAI Spot rates from India to Europe, which had risen most dramatically in the first weeks of the Iran conflict, slipped back a bit more from $3.93 per kilo at the end of April to $3.73 by 29 May.

By early June, sources suggested various other factors were helping push air freight rates up again, including upcoming abolition of de minimis rules into the EU (which had exempted small packages of up to €150 from import duties). With that change due to take effect from 1 July, some shippers were apparently rushing to shift products for Europe ahead of that date.

Sources also cited continuing strength of demand on Transpacific and inter-American lanes, while some shippers looked to move early to lock in capacity longer-term ahead of peak season.

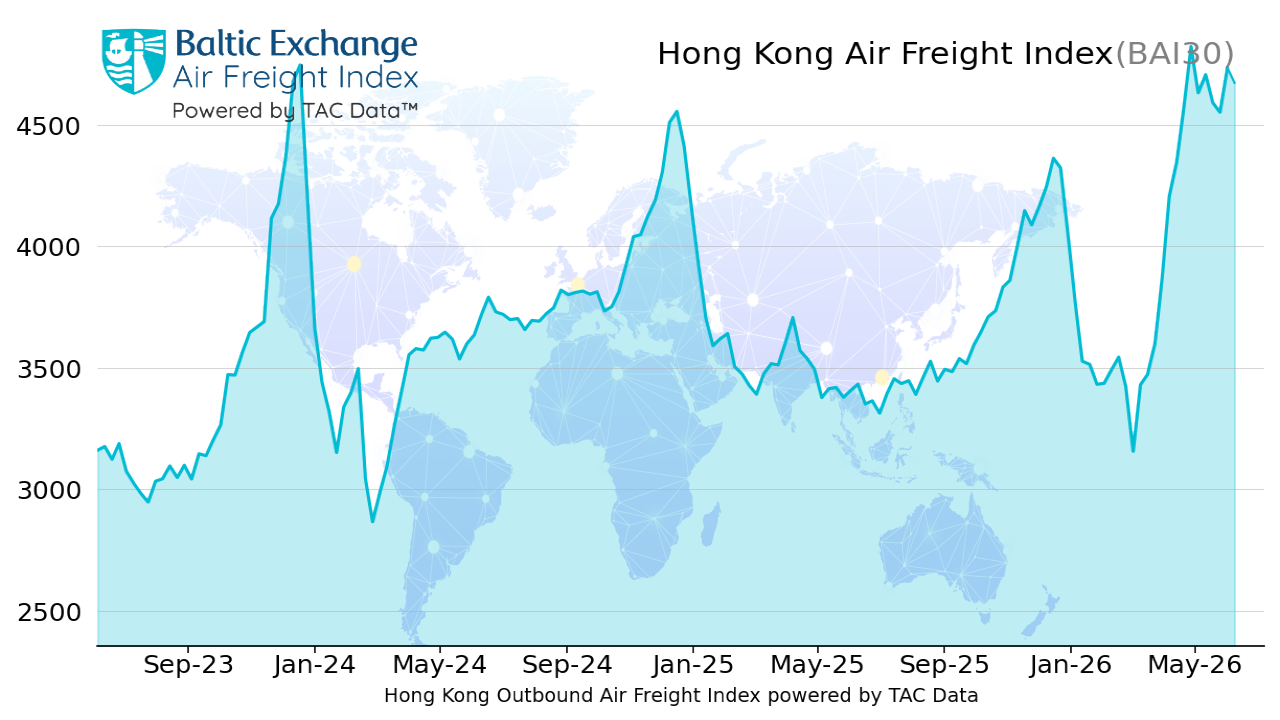

The overall index of outbound routes from Hong Kong (BAI30), reflecting the full spectrum of rates on spot and forward contracts from the world’s biggest cargo airport, actually edged up a little further by +2.2% over the four weeks to 1 June, leaving it ahead at +39.0% YoY.

The overall index of outbound routes from Hong Kong (BAI30), reflecting the full spectrum of rates on spot and forward contracts from the world’s biggest cargo airport, actually edged up a little further by +2.2% over the four weeks to 1 June, leaving it ahead at +39.0% YoY.

Outbound Shanghai (BAI80) – second only to HK by volume – eased lower by -2.3% month-on-month (MoM), although it remained +29.9% YoY.

Out of Europe, rates were more mixed. The index of outbound routes from Frankfurt (BAI20) edged lower by -4.9% MoM to 1 June, leaving it at +14.8% YoY.

Outbound London Heathrow (BAI40) gained a further +4.1% MoM, adding further to previous big gains in recent months to leave it up a whopping +71.2% YoY.

From the Americas, rates were also volatile, with the index of outbound routes from Chicago (BAI50) spiking briefly in early May but then falling back sharply to be lower some -23.4% MoM by 1 June, albeit still at +16.3% YoY and rising again in the first week of June.

From a global macro perspective, markets continued to be remarkably sanguine about potential damage caused by events in the Middle East due to rising inflation and/or a hit to growth due to the oil price shock.

On the contrary, the AI theme, which had already revived strongly in April, continued to drive markets higher in May.

This was not just reflected in the big US tech stocks – led by Nvidia, the world’s leading AI chipmaker, which actually saw its share price fall a little over the month. May also saw continued surges in the share prices of semiconductor manufacturers in Asia, including Samsung and SK Hynix in South Korea, as well as TSMC in Taiwan, helping push the total capitalisation of those stock markets to record highs.

By mid-May, Korea’s KOSPI index was up more than +200% YoY, while the Taiwan index was up more than +120% YoY and Japan’s Nikkei 225 index was up around +80% YoY.

By late May, South Korea and Taiwan had thus become the 6th and 7th largest equity markets in the world by market cap, bigger than any of the markets in Europe led by the United Kingdom, France and Germany, as well as bigger than Canada.

For many market participants this looked like a pretty seismic change, with six of the seven biggest equity markets in the world – after the US, still way ahead at the top – now being in Asia. China, Japan, Hong Kong and India, as well as South Korea and Taiwan, are all now ahead of the European markets.

These dramatic changes also posed some questions for investors going forward, given how concentrated the recent surge has been in AI-related companies, and how stock markets in Korea and Taiwan are typically driven so much by speculative retail investors, which some view as a potential warning flag.

Others, however, point to the fact that, although AI has been a key factor, there is also significant diversity at least in the Korean economy, with plenty of value in local industrial stocks like shipbuilders, defence sector exporters, healthcare and materials, as well as the financial sector.

In Taiwan, the market is much more dominated by one stock – TSMC – which has incredible pricing power as a supplier of choice to massive customers like Nvidia, AMD, Apple and Google. The biggest potential risk with Taiwan is ongoing uncertainty over its relationship to China, which is intrinsically difficult to quantify or hedge.

Nevertheless, the rise of both South Korea and Taiwan is highly evident in the TAC air freight pricing data, which continue to show very significant gains YoY both to Europe and the US.

Going forward TAC is also in the process of adding various new dimensions to the service – including TAC Explorer, providing guidance on rates for hundreds of additional lanes, as well as AI-driven reports to help explore the characteristics of each individual lane tracked. Stay tuned for more details.

Neil Wilson, TAC Editor

Neil Wilson is Editor of TAC Index, which provides independent, accurate and actionable global air freight data, allowing our customers to make comparative, cost-effective and intelligent air freight decisions.

Neil has more than 30 years’ experience in financial journalism and publishing, specialising mainly in derivatives and alternative investments. He has contributed to various publications including The Financial Times, The Economist and Risk magazine. He has also been a guest speaker at many industry events.

Neil has a B.A. with Honours in Philosophy, Politics and Economics from the University of Oxford.

Receive monthly air freight market reports direct to your inbox.