Global trade braces for sharp cooldown

ING analysts warn of a "significant slowdown" in 2026

By Carly Fields

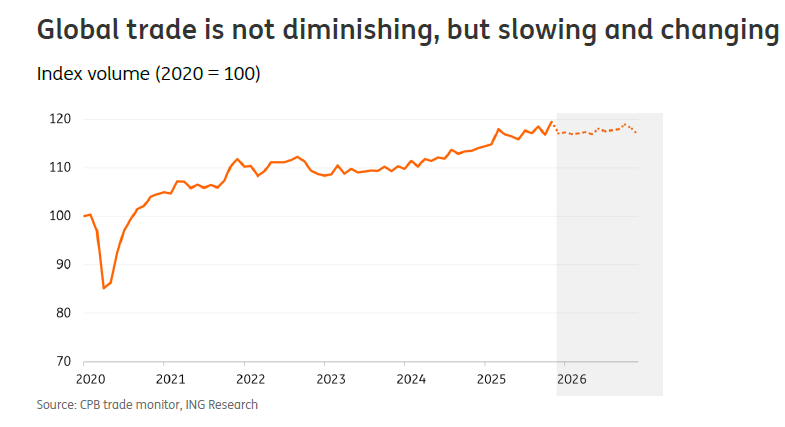

As the dust settles on a historic year of upheaval, the global trade landscape is bracing for a starkly different reality in 2026. After a surprising 4.2% year-over-year expansion in 2025, economists at ING are forecasting a "significant slowdown” for 2026 with growth projected to plummet to a range of just 0.5% to 1% for the coming year. This cooling-off marks the end of a chaotic adjustment period and the beginning of what analysts are calling a new era of "lasting volatility".

The message is clear: the resilience that defined the past year is being tested by a toxic mix of protectionism and geopolitical manoeuvring. According to the report authors, ING junior economist Julian Geib and ING senior sector economist, transport and logistics Rico Luman,

2025 will be remembered as "the year everything changed in global trade".

The primary catalyst for this shift was the sweeping set of tariffs announced by US President Donald Trump in April 2025, enacted via the International Emergency Economic Powers Act (IEEPA). While these measures initially sparked a wave of frontloading as importers rushed to secure goods before price hikes took hold, that artificial boost has now evaporated, leaving a vacuum in its wake.

"Geopolitics continues to prevail over efficiency, and protectionism remains firmly in place," the authors note, highlighting a fundamental shift in the global order. The era where supply chains were optimised solely for cost-effectiveness appears to be over. Instead, trade is now being used as a strategic tool of foreign policy. The start of 2026 has already been characterised by this trend, notes ING, with the US administration escalating efforts to assert control over Greenland and threatening European partners with fresh tariffs.

Death knell for free trade

The impact of this "crackdown on free trade" is being felt unevenly across the globe. While the world's largest economy, the US, represents about 14% of global imports, many Chinese exporters have proven remarkably adept at pivoting to new markets. In fact, China surpassed the US as Germany’s largest trading partner in 2025, a shift driven by Chinese firms stepping into traditional German strongholds like automotive, pharmaceuticals, and industrial components. Conversely, the eurozone has struggled, with high energy costs weighing heavily on industrial exports.

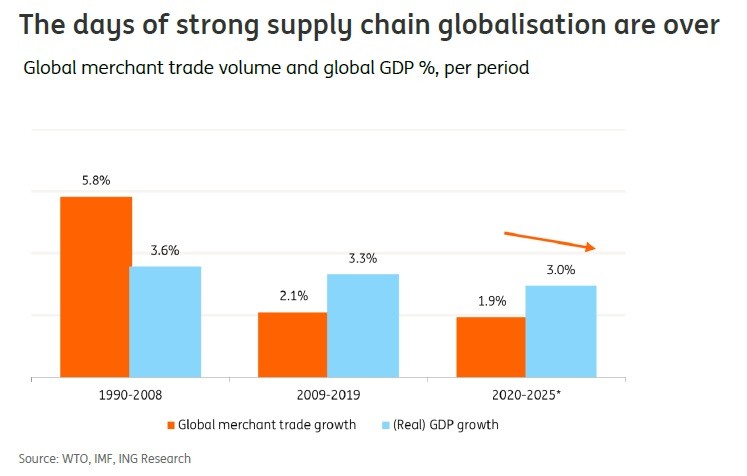

Beneath this lies a deeper structural transformation.

The report suggests that "global imbalances seem to have reached their limits".

The rapid globalisation of the 1990s, which brought economic benefits, also created deep-seated dependencies that are now being viewed as liabilities. As nations prioritise risk management over pure efficiency, trade growth is increasingly lagging behind overall GDP growth, a trend that has been building for several years but is now being accelerated by rising protectionism.

This year is also set to be critical for established trade frameworks. The report points to the upcoming review of the United States-Mexico-Canada Agreement (USMCA) as a "key trade event". Recent official statements have even "hinted at the possibility of the deal lapsing altogether" or being dismantled in favour of separate bilateral agreements. This uncertainty, combined with the expiration of the US-China trade deal in October 2026, ensures that "volatility is here to stay".

For businesses and investors, the message is one of caution. Corporate insolvencies are on the rise, particularly in export-reliant sectors like construction, retail, and automotive. In the US and China, the temporary protection offered by tariffs in 2025 is expected to wear off, potentially leading to insolvency increases of 8% and 10% respectively. As the ING analysis concludes, "the impact of the emerging global order will be felt in 2026” as the world navigates a period of "greater fragmentation" and tempered expectations.

Mayhem for metals

A trade sector that is particularly susceptible to geopolitics is global metals. According to Ewa Manthey, commodities strategist at ING, the global metals market is entering a transformative and highly volatile era, marking its most significant shift since the China-led super-cycle of the early 2000s. Manthey notes that the coming metals ‘cycle’ will be defined by a "more fragmented, policy-driven and geopolitically-charged market" where traditional economic drivers are being superseded by strategic national interests.

A primary catalyst for this shift is the diversification of demand.

While China remains a major player, it "no longer dominates global metals demand as it once did".

Instead, consumption is becoming increasingly sector-specific, fuelled by the rapid expansion of electrification, defence spending, and data infrastructure. This has led to historic rallies, with silver surpassing $80/oz for the first time in history and copper climbing 42% in 2025.

Supply dynamics are also tightening as "resource nationalism has become a defining feature of metals markets", Manthey said. Governments are moving to secure strategic materials through export bans and aggressive stockpiling. For instance, the US Pentagon is seeking to procure up to $1 billion in critical minerals to counter over-reliance on single suppliers. Similarly, the European Union’s new RESourceEU Action Plan will begin joint purchasing and stockpiling initiatives in 2026.

Manthey warns that these forces will result in a market where "tightness persists longer, price spikes are more likely, and volatility is structurally higher".

For trade professionals, 2026 represents a definitive departure from the past for metals, characterised by "constrained and politicised supply".