BAI Index July 2026: Gulf ceasefire eases pressure on jet fuel, but air freight rates stay firm through June

Despite a well-anticipated memorandum of understanding (MoU) to end the war in the Middle East between the US and Iran, global air freight rates continued to climb through most of June.

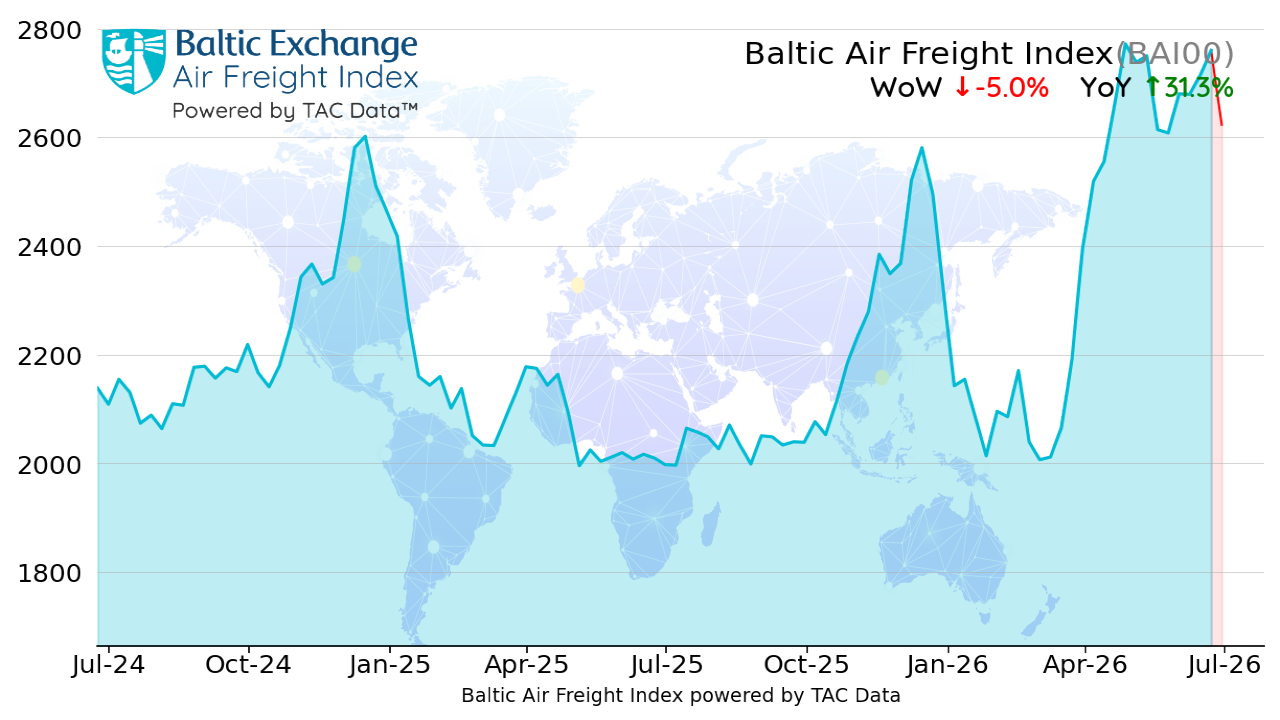

The global Baltic Air Freight Index (BAI00), calculated by TAC Data, gained a further +5.8% over the four weeks to 22 June, leaving it ahead by some +37.3% from 12 months earlier. This meant that, despite a subsequent fall of -5.0% in the week to 29 June, rates remained higher by +31.1% year-on-year.

The global Baltic Air Freight Index (BAI00), calculated by TAC Data, gained a further +5.8% over the four weeks to 22 June, leaving it ahead by some +37.3% from 12 months earlier. This meant that, despite a subsequent fall of -5.0% in the week to 29 June, rates remained higher by +31.1% year-on-year.

That was still above levels even at the very highest points of the previous three peak seasons and only exceeded in the past during the Covid pandemic when passenger bellyhold capacity was severely disrupted.

The formal announcement of the MoU draft did not come until 14 June and not signed until 17 June. Nevertheless, crude oil and jet fuel prices had already started to fall sharply in anticipation of the agreement.

The price of Brent crude fell from over $95 per barrel at the start of the month to under $80 by 16 June. The price of jet fuel, according to the IATA Jet Fuel Price Monitor, based on Platts data, had plummeted some -26% by 26 June from the previous month’s average.

Jet fuel prices remained up some +29.5% from the previous year, according to the Platts data, but had clearly eased a great deal from the extreme levels of March and April when the ‘crack spread’ between crude and jet widened dramatically.

Nevertheless, this big fallback in jet fuel prices did not seem to feed through very quickly into lower air freight rates.

BAI Spot rates out of Hong Kong had started the month on a firmer note, rising again in the first part of June, before starting to fall back in the latter part of the month. BAI Spot from HK to Europe ended May at HK$44.54 per kilo and was still at HK$42.53 by 30 June.

BAI Spot rates out of Hong Kong had started the month on a firmer note, rising again in the first part of June, before starting to fall back in the latter part of the month. BAI Spot from HK to Europe ended May at HK$44.54 per kilo and was still at HK$42.53 by 30 June.

BAI Spot from HK to the US East Coast had been $55.54 at the end of May and was still at $53.49 by 30 June. Likewise, HK to the US West Coast began June at HK$51.71 and was still at HK$49.43 by the end of the month.

The overall index of outbound routes from Hong Kong (BAI30) – reflecting the full spectrum of spot and forward rates being paid across multiple lanes from the world’s biggest cargo airport – also edged higher, rising +4.5% over four weeks to 22 June, leaving it up +41.4% year-on-year (YoY). Despite falling the following week, it was still at +34.1% YoY by 29 June.

Similarly, outbound Shanghai (BAI80) was almost unchanged over the month to 29 June and +37.0% YoY.

Rates out of Europe were more mixed. The index of outbound routes from Frankfurt (BAI20) gained +14.3% over the four weeks to 29 June, leaving it at +27.9% YoY.

By contrast, outbound London Heathrow (BAI40) shed some -20.9% month-on-month (MoM) to 29 June, giving back a big chunk of its gains from recent months and leaving it up only +1.8% YoY.

Out of the Americas, the index of outbound routes from Chicago (BAI50) gained +5.5% MoM to 29 June 29, leaving it at +34.9% YoY.

Clearly, it was taking some time for lower jet fuel prices to feed through to air freight rates, which is not surprising given that many carriers were perhaps still flying planes using fuel they had contracted to buy at those recent higher prices.

Clearly, it was taking some time for lower jet fuel prices to feed through to air freight rates, which is not surprising given that many carriers were perhaps still flying planes using fuel they had contracted to buy at those recent higher prices.

However, sources were also suggesting various other factors were helping keep air freight rates up. As we noted last month, one specific factor was the abolition of de minimis rules into the European Union (which had exempted packages of up to €150 from import duties) that takes effect on 1 July, with some shippers rushing to shift products for Europe ahead of that date.

Oher sources had also cited the continuing strength of demand on Transpacific and inter-American lanes, with some shippers looking to move early to lock in capacity longer-term ahead of peak season.

Looking ahead, however, sources were also anticipating that prices must start to ease much further – so long as the ceasefire in the Gulf held – even if it would probably take many weeks or months for the market to get back to normal prior to the outbreak of the US-Iran war. Indeed, it seemed quite likely rates may continue to price in a risk premium all the way through to peak season.

Meanwhile, from a macroeconomic perspective, equity markets continued to rise higher, driven by the growing demand for Artificial Intelligence infrastructure. That was despite some wobbles in June, notably in the tech-heavy Nasdaq Composite index in the runup to the blockbuster IPO of Elon Musk’s Space Exploration Technologies Corp, better known as SpaceX.

The SpaceX IPO was seen as remarkable in many ways – not least for placing such a stratospheric valuation on a company that has hitherto made billions of dollars of losses and where the business case seems to depend at least partly on data centres yet to be built on Mars.

Predictably, SpaceX shares initially soared after launch but soon suffered the second biggest ever single-day decline in value any stock has ever recorded on 22 June (dropping about $400 billion).

With Anthropic, Open AI and others also lining up huge IPOs – plus existing players like Google looking to raise massive amounts of extra capital to fund investments in AI – the AI theme looks set to roll on.

Most investors, at least for now, seem to expect capital markets to keep the funding coming, although some are cautioning that this AI party must eventually reach a conclusion at some point.

In the meantime, however, air freight rates – despite that recent fall in jet fuel prices, which must surely start to feed through more fully soon – are continuing to look pretty firm.

Going forward TAC is also in the process of adding various new dimensions to the service – including TAC Explorer, providing guidance on rates for hundreds of additional lanes, as well as AI-driven reports to help explore the characteristics of each individual lane tracked. Stay tuned for more details.

Neil Wilson, TAC Editor

Neil Wilson is Editor of TAC Index, which provides independent, accurate and actionable global air freight data, allowing our customers to make comparative, cost-effective and intelligent air freight decisions.

Neil has more than 30 years’ experience in financial journalism and publishing, specialising mainly in derivatives and alternative investments. He has contributed to various publications including The Financial Times, The Economist and Risk magazine. He has also been a guest speaker at many industry events.

Neil has a B.A. with Honours in Philosophy, Politics and Economics from the University of Oxford.

Receive monthly air freight market reports direct to your inbox.