Tech: trade’s saviour in 2026?

Movements of AI-enabling goods could offset the negative effects of the Middle East conflict

By Carly Fields

The global trading system looks set to be defined by a tug-of-war between high-tech acceleration and geopolitical disruption through to 2027.

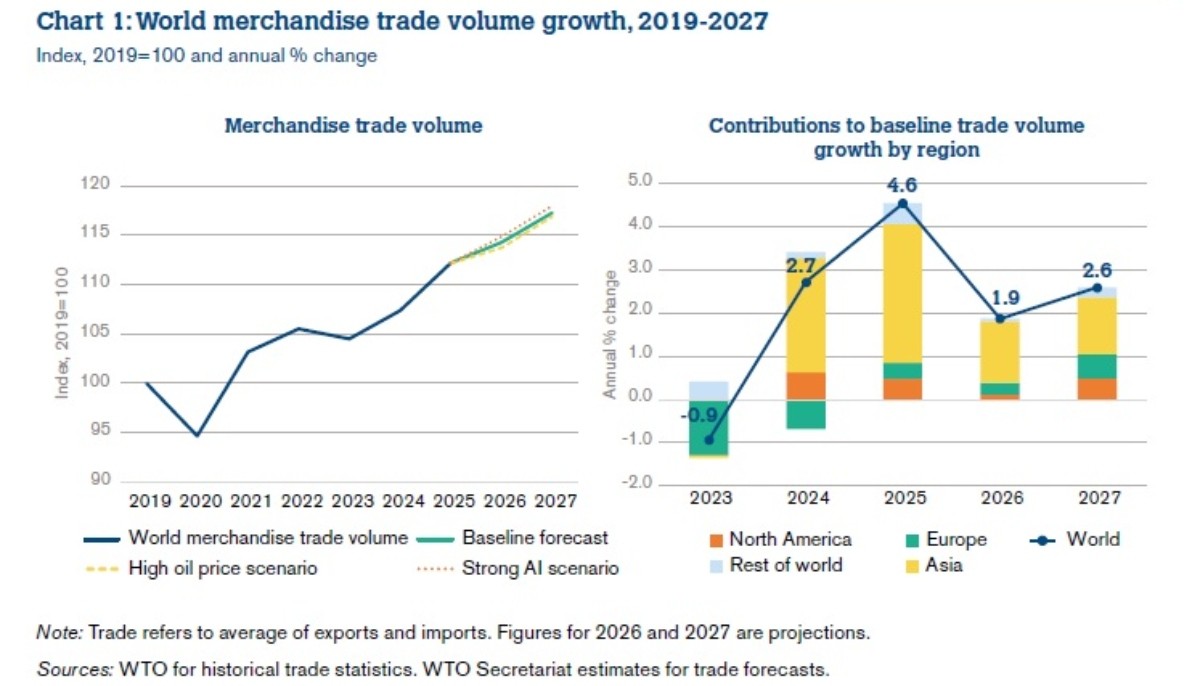

According to the latest Global Trade Outlook and Statistics report released by the World Trade Organization (WTO), world trade is projected to slow in 2026 following a 2025 performance that defied many expert predictions. While 2025 saw a robust 4.6% expansion in merchandise trade volume, current baseline projections suggest this growth will dip to 1.9% in 2026 before seeing a modest recovery to 2.6% in 2027.

Robert Staiger, the WTO’s chief economist, notes that the current landscape is being pulled in two directions by "powerful and opposite forces". He explains that "on the one hand, the extraordinary momentum of investment in artificial intelligence (AI) continues to energise global demand for high-tech goods and digitally delivered services”, while "on the other hand, the conflict in the Middle East—and the resulting spike in energy and transport costs—could weigh heavily on world trade and output". This duality is the central theme of the 2026 outlook, as the global economy attempts to maintain momentum amid a deepening energy shock and shifting policy regimes.

The resilience seen in 2025 was largely built on temporary foundations, according to the report.

North America, for instance, experienced a significant wave of "frontloading" in the first half of 2025, as importers rushed to bring in goods—particularly pharmaceuticals and gold—ahead of anticipated reciprocal tariff increases by the US. This surge was bolstered by the ongoing AI investment boom, where "hyperscaler" firms in North America and across Asia drove massive demand for data centre infrastructure and advanced processors.

However, these factors are expected to provide less of a tailwind this year. Staiger cautioned that "some of the factors behind that resilience—such as frontloading of imports ahead of tariff hikes, and investment in AI-related infrastructure—are expected to be absent or reduced this year".

Middle East challenge

The most immediate threat to the WTO’s baseline forecast is the escalating conflict in the Middle East. The disruption of oil shipments through the Persian Gulf, a region that accounted for 20% of global liquid petroleum consumption in 2024, has sent crude oil prices climbing toward $100 per barrel. WTO economists warn that if these high prices prevail, the already slowing merchandise trade growth of 1.9% could be shaved down by another 0.5 percentage points to just 1.4%.

The services sector is equally vulnerable, particularly in transport and travel, which could see growth reduced by 0.7 percentage points due to regional instability and structurally elevated fuel costs.

This energy shock is also rippling through agricultural supply chains. The Persian Gulf is a primary source of fertiliser for many major agricultural producers. For example, India and Thailand rely on the region for 40% and 70% of their urea imports, respectively. A supply shock in these markets transmits price signals globally, potentially affecting food security and trade in agricultural commodities far beyond the immediate conflict zone.

Despite these headwinds, the AI revolution remains a strong upside risk, according to the WTO.

AI-enabling goods have seen their share of global merchandise trade increase sharply, acting as an "engine of trade expansion" even as traditional goods categories remain subdued. WTO analysis indicates that if AI-related spending remains exceptionally strong through 2026, it could offset the negative effects of the Middle East conflict, potentially boosting merchandise trade growth back up to 2.4%.

The high import intensity of AI investment—estimated at 70-90% for computer equipment compared to less than 2% for construction—means that every dollar of AI investment has a disproportionately large impact on global trade flows.

On the regional level, Asia continues to be the dominant engine of growth, contributing a staggering 71% of total world merchandise trade volume growth in 2025. China’s export volume grew by 9.2% last year, as the country re-oriented its trade toward fast-growing emerging markets in Africa and South America to compensate for weakening demand and higher tariffs in the US.

While the direct trade link between the world's two largest economies has frayed—with US imports from China falling 29% in 2025—the WTO report highlights that some of this trade is likely being rerouted through third countries or adjusted via complex global value chains.

Return to stability

As the world looks toward 2027, the baseline expectation is for a return to more stable medium-term trends, with trade growth picking up to 2.6% for merchandise and 5.1% for services.

However, the landscape remains fundamentally altered. The share of world trade conducted on the WTO’s non-discrimination principle of Most-Favoured-Nation (MFN) treatment fell to roughly 72% by early 2026, reflecting a proliferation of regional agreements and unilateral tariff actions.

Ultimately, the trajectory of global trade over the next two years will depend on which of Staiger’s "opposite forces" prevails. If the AI boom continues to propel demand and the energy shock remains contained, the global trading system may pass through this period of uncertainty with agility. However, a prolonged conflict in the Middle East combined with deepening trade fragmentation could see the 2026 slowdown become more pronounced.

As Staiger concludes, the key questions remain whether the AI surge can sustain its pace and if trade fragmentation pressures will finally stabilise or continue to deepen.